|

Back to Blog

Read Peter Oakes's Media Contributions31/12/2024  February 03, 2023

In Malta, AML Failures Trigger Penalties Against Local Cryptocurrency Platforms ACAMS MoneyLaundering.com January 12, 2023 Jack Ma profile: how China is making the Alibaba and Ant Group founder pay for his outspoken stance Business Post November 22, 2022 Louth MEP says tech job losses ‘shouldn’t be too much of concern’ as fintech future ‘looks bright’ Independent September 23, 2022 Is the party over? Irish tech braces for a shock as the easy money dries up Business Post September 15, 2022 What will happen to money in the United Kingdom? [Radio] Newstalk September 15, 2022 Financial Leadership Summit future-proofs CFOs Irish Times August 27, 2022 The Fintech 15: the people making waves in one of Ireland’s leading tech sectors Business Post June 17, 2022 Tide turns on crypto currencies as recession fears stalk markets Irish Times May 11, 2021 To Combat ‘Severe Consequences’ of De-risking, EU Wants Better Risk Assessments ACAMS MoneyLaundering.com April 10, 2022 ‘Defensive’ attitude of Central Bank putting off fintech investors Business Post March 30, 2022 Revolut rival Vivid withdraws application for Irish e-money licence Irish Times March 22, 2022 EU AML Supervisors Disregarding Risk-based Approach ACAMS MoneyLaundering.com February 24, 2022 Irish-based expats adviser Abbey Wealth changes hands in CEO-led buyout Irish Times December 9, 2021 Increasing competition in the digital payments market RTE July 13, 2021 Banks Small in Stature, High in Risk Could Escape Direct EU Oversight ACAMS MoneyLaundering.com June 11, 2021 Ireland’s new biggest bank: How Barclays rose to the top Irish Times March 21, 2022 Winklevoss twins secure Irish e-money licence for Gemini Payments Irish Times October 22, 2020 Leveris Core Interview with Peter Oakes, Founder and FinTech Mentor at FinTech Ireland (Thought Leadership) Irish Tech News October 14, 2020 An Abundance of Financial Innovation (Thought Leadership) Soldo September 25, 2020 FinCEN Files: Scale of challenge facing financial regulators revealed in leaked documents Irish Times September 3, 2020 Banks Should Review Client Onboarded Remotely During Pandemic: Moneyval ACAMS MoneyLaundering.com June 11, 2020 The Irish Fintech Ecosystem: Headwinds and Tailwinds & the Making of a Global Fintech Centre (Thought Leadership) CPA Ireland Journal April 22, 2020 How to operate as a non-executive director of regulated firms [Podcast] Captivated Audience Podcast February 14, 2020 European Supervisors Instructed to Challenge Banks More Frequently ACAMS MoneyLaundering.com December 5, 2019 EU inches towards uniform AML rules and supervision ACAMS MoneyLaundering.com September 24, 2018 Ireland at the crossroads as prosperity and Brexit approach Australian Financial Review September 14, 2019 Bank to the future online banking set for big changes RTE September 12, 2018 EU Officials Pitch Expanded AML Oversight Role for European Banking Authority ACAMS MoneyLaundering.com August 31, 2018 The future of cash RTE June 17, 2019 Brexit: Bane of Banks and Bank Regulators alike ACAMS MoneyLaundering.com April 26, 2018 GDPR: where does it sit in the cyber security mix? Irish Times April 26, 2018 Cashing in on digital ‘wallets’ Irish Times March 11, 2018 Roubles rumbled: What we don't know about Russian money in the IFSC Irish Times January 28, 2018 Your Business: The future of money. It’s official: cash is no longer king Business Post January 9, 2018 Irish Regulator Proposes Holding Bank Managers Liable for AML Lapses ACAMS MoneyLaundering.com October 15, 2017 Beware Bitcoin Funding-Investment Mania Investors Told Independent.ie October 11, 2017 Small companies cheer sought after tax cut Independent August 13, 2017 Former Central Bank director and lawyer join Corlytics board Business Post July 23, 2017 Australia’s Ignition to open in Dublin - appoints Peter Oakes to advise on raising an additional €2 million Business Post June 07, 2017 Fintech Ireland event at the NCI to highlight work of Ireland’s financial innovators Business & Finance June 06, 2017 Peter Oakes joins the Advisory Committee of Kyckr (Global KYC Experts to Promote and Advise Kyckr) ASX May 21, 2017 Fintech fliers - Former Central Banker Peter Oakes and software engineering manager Dave Anderson of Fintech Ireland pick ten of the up-and-coming businesses to watch out for Business Post April 30, 2017 Money laundering: was AIB’s fine too low? AIB’s €2.275 million fine raises questions about Ireland’s laws – and the Central Bank’s enforcement approach Business Post March 20, 2017 Brexit & Regulatory Arbitrage and the fintech opportunities for Ireland [Radio] Newstalk February 5, 2017 Trump v Ireland Inc: How "America First" is being felt in Ireland Business Post February 5, 2017 Former central banker warns of danger in US regulatory rollbacks. Peter Oakes has said Irish banking needs to exercise caution after Trump's Dodd-Frank comments Business Post January 5, 2017 Why 2017 could be the year the 'robo-advisors' finally come to town Fora October 16, 2016 Vast slew of public settlements now due. The Central Bank could ramp up enforcement cases before the end of the year (Thought Leadership) Business Post October 4, 2016 Former Central Bank enforcement director in private sector move. TransferMate appoints Peter Oakes to board Business Post July 28, 2016 CEO Q&A: Peter Oakes on Challenges & Opportunities for Ireland’s fintech Industry (Thought Leadership) Business & Finance July 14, 2016 Fintech has a place within financial service ecosystem Irish Times July 13, 2016 No company is immune from data security threat Irish Times July 13, 2016 The CEO Interview, Peter Oakes, Founder of Fintech Ireland - Business & Finance (Thought Leadership) Business & Finance July 5, 2016 Powering forward: Peter Oakes discusses the prospects for Ireland’s fast growth fintech industry (Thought Leadership) Business & Finance July 3, 2016 Brexit: Leave result has thrown Britain’s financial world into a tailspin Business Post July 3, 2016 Summit looks at all aspects of Internet of Things Business Post June 26, 2016 Ireland falls short in enforcing money‐ laundering laws Independent June 7, 2016 Announcement of the Fintech20 Ireland Irish Tech News June 7, 2016 Fintech Ireland event at the NCI to highlight work of Ireland’s financial innovators Business & Finance June 1, 2016 Powering forward - growth prospects for innovative disrupters (Thought Leadership) Business & Finance May 19, 2016 Viewpoint The Variable Mortgage Rates Bill (Thought Leadership) Finance Dublin April 26, 2016 FBFSS Summit: Trust is the key to a digital future - In just 10 years we could be buying driverless car insurance from Google Business Post April 24, 2016 Fintech: More than Just a Marriage of Finance and Technology (Irish Times/Grant Thornton) (Thought Leadership) Irish Times (#GTech) March 13, 2016 Central Bank fires warning shot across stockbrokers’ bows. Concerns include personal account dealing, gifts and entertainment, and intragroup relationships Business Post January 31, 2016 Irish fintech sector is banking on boom Independent January 31, 2016 Has the Central Bank’s do-nothing culture changed? It's tough to find an answer to the question: What have we learned? Business Post January 01, 2016 Irish Australian Chamber of Commerce launches Irish chapter RTE May 31, 2015 Oakes heads for high frequency trader Business Post May 28, 2015 Presentation on Fintech to Financial Services Ireland (Thought Leadership) Financial Services Ireland April 22, 2015 Ireland plays for high stakes in fintech game Business Post April 22, 2015 Central Bank: Behind closed doors Business Post March 3, 2015 Presentation - Big Opportunities in Fintech (Thought Leadership) UK Trade & Investment October 7, 2014 Restrictions on the loan to value and loan to income ratios for house purchase [Radio] Part 1 / Part 2 NewsTalk with Ivan Yates September 13, 2014 The Future of Money [Radio] RTE August 8, 2014 Mortgages – Consumer Protection and Prudential debate [Radio] Part 1 / Part 2 NewsTalk with Ivan Yates July 6, 2014 Any debt deal will cover just 8pc of our €64bn loan Independent July 5, 2014 IMF & EU debt deal for Ireland [Radio] Part 1 / Part 2 / Part 3 RTE with Claire Byrne July 4, 2014 Digital currencies and other regulatory issues [Radio] Newstalk with Ian Guider January 9, 2013 The Enforcement Directorate at the Central Bank under Peter Oakes (Ian Guider and Jon Ihle) [Radio] Newstalk April 9, 2013 COMMENT: Elderfield's departure no surprise Business Post January 13, 2013 Market Week – Oakes Leaving Central Bank Business Post January 8, 2013 Oakes to step down from Central Bank Business Post January 8, 2013 Central Bank's director of enforcement to step down RTE December 11, 2012 Address by Director of Enforcement, Peter Oakes to Central Bank Enforcement Conference Speech (Thought Leadership) Central Bank of Ireland November 22, 2012 ICON fined €10,000 by Central Bank for breaches of market abuse rules RTE May 8, 2012 Address by Peter Oakes, Director of Enforcement, to the Association of Compliance Officers (‘The role of enforcement and activities of the Enforcement Directorate’) (Thought Leadership) Central Bank of Ireland November 19, 2012 Ulster Bank fined €1.96m for breaches of financial regulations RTE October 4, 2012 Central Bank fines Bank of Ireland Mortgage Bank for breaches RTE June 21, 2012 UBS fined for anti-money laundering breaches RTE April 2, 2012 Central Bank fines life company (Alico) more than €3 million. The Central Bank has fined a life company €3.2 million for breaches of financial regulation. Business Post March 18, 2012 CHC investors could face long delay on payout Business Post January 22, 2012 The financial heads that didn't roll Business Post December 19, 2011 Insurance firm may have to refund €2m RTE December 11, 2011 Another broker in line for censure Business Post July 22, 2011 Central Bank fines Aviva Investors Ireland RTE June 9, 2011 Central Bank to give pre-crisis directors initial written warning Independent April 9, 2011 Financial Regulator to begin flexing its new muscles Business Post June 28, 2010 Key appointments made at Central Bank RTE April 17, 2010 Banks seek loopholes to escape tracker mortgages Business Post March 02, 2009 New banking oversight commission planned RTE December 5, 2009 The Inquisitor: Honohan’s home truths rattle the bankers’ cages Business Post June 30, 2007 FitzPatrick rails against ‘corporate McCarthyism’ Business Post September 23, 2006 Customers take hits from scams Business Post July 30, 2005 Are 100% mortgages a fraud risk? Business Post

0 Comments

Back to Blog

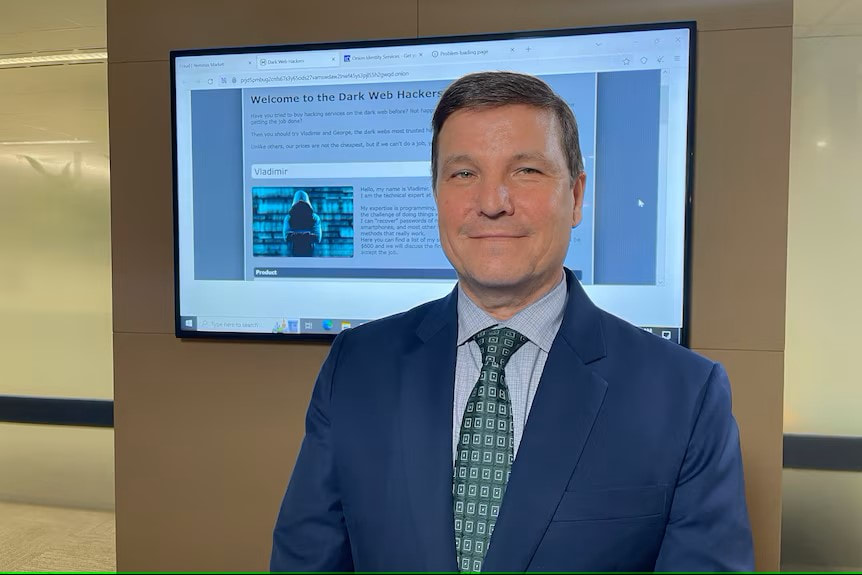

Interesting to see that while the cost for fake/stolen passports and drivers licences have increased (almost double), the cost to hack someone’s email account dropped 60% in 2023. At least there is no escaping the laws of economics for bad actors! See this YouTube link for more - https://www.youtube.com/watch?v=MWb7dUUXO2M "Inflation is hitting everyone hard it seems — even scammers. New data reveals the cost of fake or stolen documents like passports and driver's licenses on the dark web has gone up significantly, as demand increases and the number of people being scammed decreases. According to a report from accounting firm BDO, the average cost of buying a fake or stolen passport on the dark web is now $2,372 (up from $1,399 in the previous quarter), while a driver's license will set you back $844 (up from $465). But it's a competitive market and in some cases prices have dropped. The average cost to hack into someone's email is now just $262 (down from $668), according to BDO.".  BDO's Stan Gallo said the dark web is “like any other market environment where there's supply and demand". "He believes increased awareness of scams over the past year, high profile crackdowns and more embedded security measures in some ID documents has made it harder for criminals to get away with obtaining, selling and using fraudulent documents and has therefore pushed the price up.

"It's like any other market environment where there's supply and demand," he told the ABC. "And if there's a restricted supply and the demand is still there, then the price goes up. If things are easier to get, then the price will come down because it will drive competition." He notes anyone who tries to buy fake passports or conduct other illegal activities on the dark web must accept a significant risk and face repercussions including possible imprisonment.". Read more here https://www.abc.net.au/news/2024-03-25/criminal-inflation-stolen-data-price-increase-dark-web-scams/103620916

Back to Blog

Click here to LISTEN

The funeral of Queen Elizabeth the Second is happening on Monday, with the mourning period continuing up until that day. Soon after that, final decisions will be made surrounding the currency, and the changing of notes depicting the Queen’s head, to King Charles III’s head. Peter Oakes is a business consultant, Board Director of TransferMate, formerly of the Central Bank, joined Kieran on the show to discuss the process. Click here to LISTEN Linkedin Post HERE

Back to Blog

16 January 2021: Peter Oakes has again being recognised as a leading fintech consultant for 2021 following his listing in 2020.

Chambers and Partners released its Fintech Rankings for Ireland in January 2021. Peter is the only individual / boutique professional services firm (CompliReg) to be ranked along side some of Ireland's largest consulting firms. In research carried out by Chambers and Partners, Peter's clients and fintech industry experts informed the researchers that:

Reach to Peter for assistance and advice via the details on our contact page. Further reading:

Back to Blog

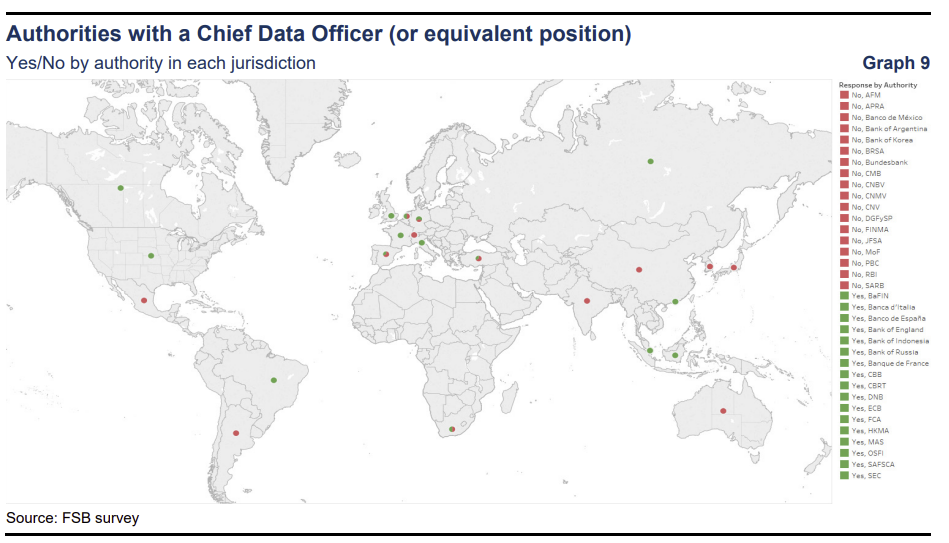

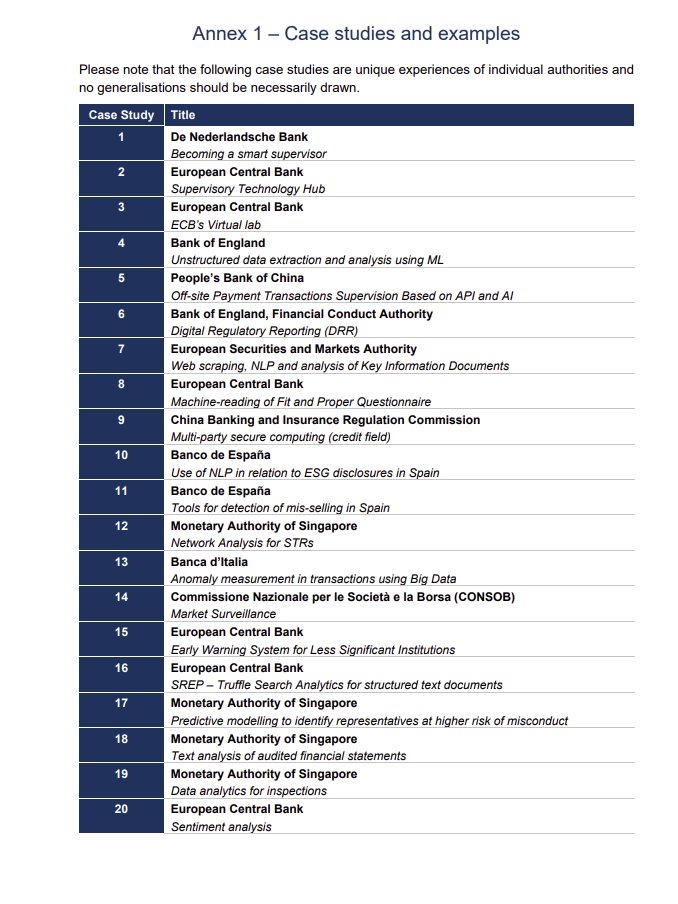

Download Report - The Use of Supervisory and Regulatory Technology by Authorities and Regulated Institutions Market developments and financial stability implications One for all the #regtech and #suptech ambassadors / champions in the network (and you may have spotted it) - Use of Supervisory and Regulatory Technology by Authorities and Regulated Institutions covering:

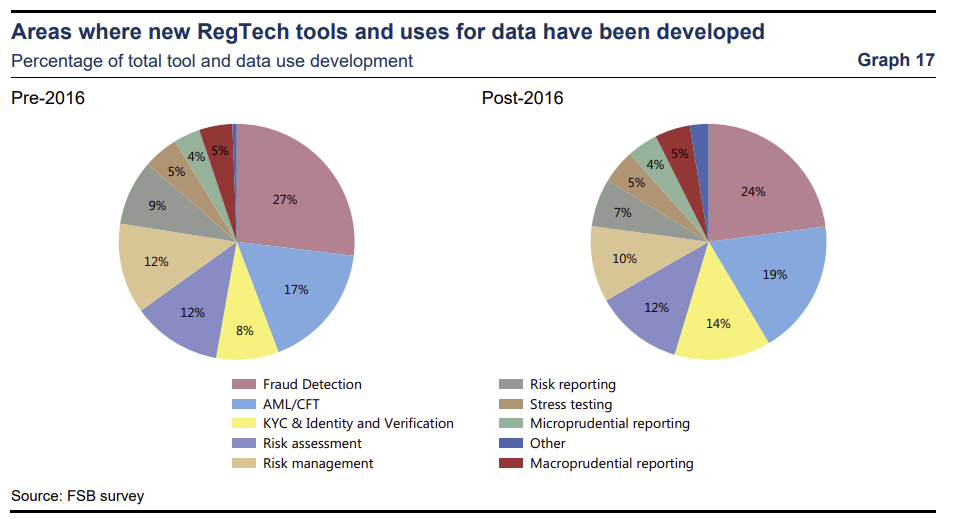

As you will see in the images below and in the report, less than 50% of supervisory authorities responding to the FSB survey had a Chief Data Officer or equivalent. Areas where new RegTech tools and uses for data have been developed post 2016 are:

Whereas pre-2016, the supervisory authorities were focused on:

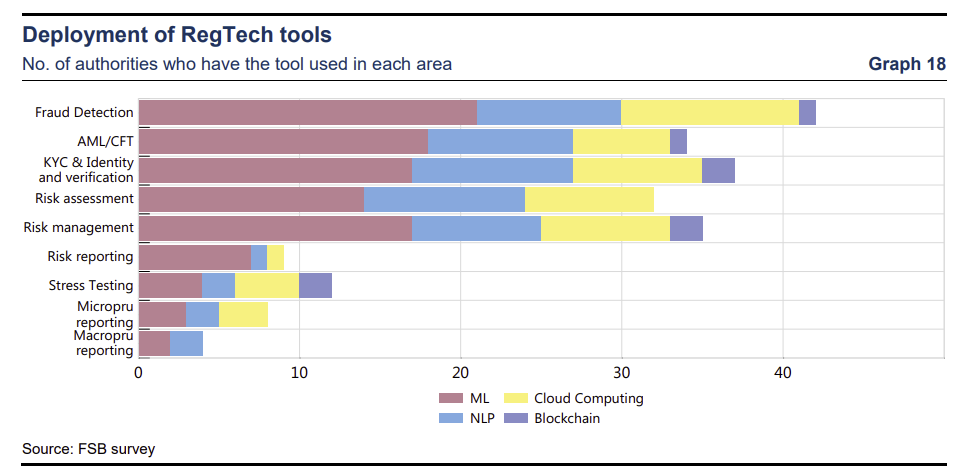

Future technology use by the regulator I thought the section 9.2 Future technology use by the was regulator interesting. The FSB reports that rapid changes to the financial landscape and evolving market structure could be accompanied by changes in supervisory surveillance techniques. [Oakes - Ok so that is relatively obvious] 85% + of survey respondents expect that the continued evolution of available technologies will result in changes to supervisory processes, with 68% expecting this to be a considerable change. However, authorities expressed concern that undue reliance on SupTech tools could lead to misplaced focus on areas where risks can be easily measured. [Oakes - so just because you can do something doesn't mean you should do it]. This may deflect attention from areas of concern that are not as easily given to quantifiable measurement [Oakes - so true]. Retaining a forward-looking human based supervisory process Thus while authorities may recognise the importance of integrating technology into their supervisory approaches, they could also acknowledge the importance of retaining a forward-looking human based supervisory process. The modern supervisory philosophy in most jurisdictions surveyed is based on predictive and human judgement-based oversight of regulated institutions. Technology offers the opportunity to automate routine tasks, develop new analytical techniques and provide better information. Using tools such as AI and ML to analyse increasing volumes of regulatory data provides opportunities for authorities to shift their focus to those aspects where humans excel over machines, e.g. judgement-based decision making. [Oakes- couldn't add anything further to that]. Cases Studies I also recommend a read of Annex 1 where the Case studies and examples are contained. There are case studies from 26 supervisory authorities:

Source: https://www.fsb.org/2020/10/the-use-of-supervisory-and-regulatory-technology-by-authorities-and-regulated-institutions-market-developments-and-financial-stability-implications/ https://www.fsb.org/2020/10/the-use-of-supervisory-and-regulatory-technology-by-authorities-and-regulated-institutions-market-developments-and-financial-stability-implications/

Back to Blog

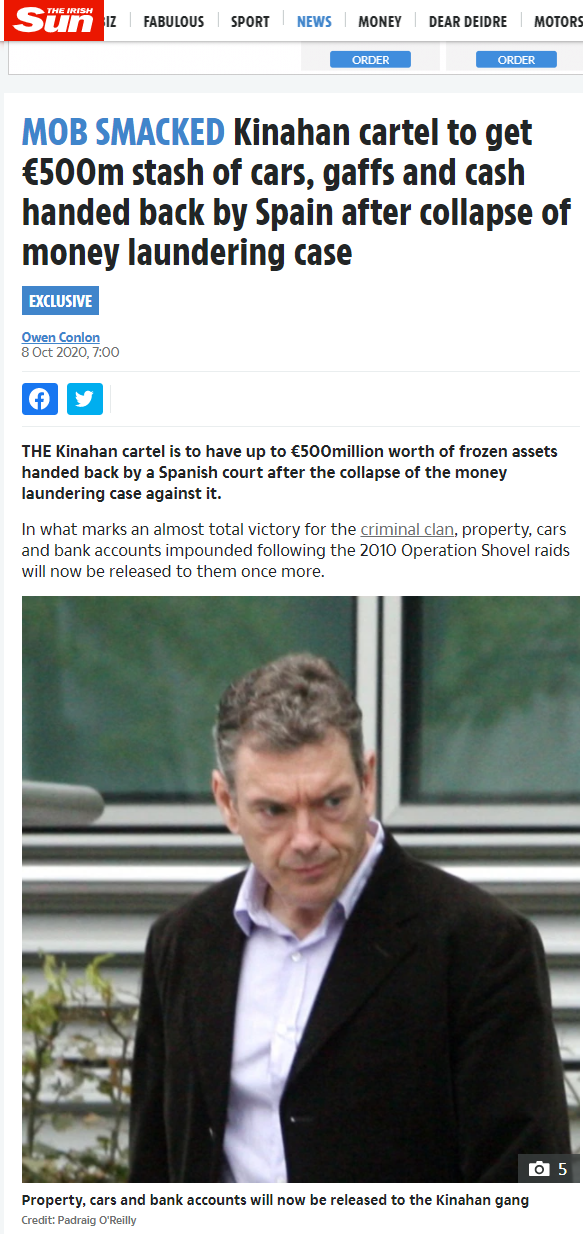

Here's one for the #moneylaundering typology case studies for #MLROs as part of regulatory training requirements!

Relates to the collapse of major investigation into the Kinahan cartel and more than half a billion euros- particularly €500,000,000 stash of cars, properties & cash handed back to the accused by a Spanish judge after collapse of money laundering case. Continue reading at CompliReg by clicking here.

Back to Blog

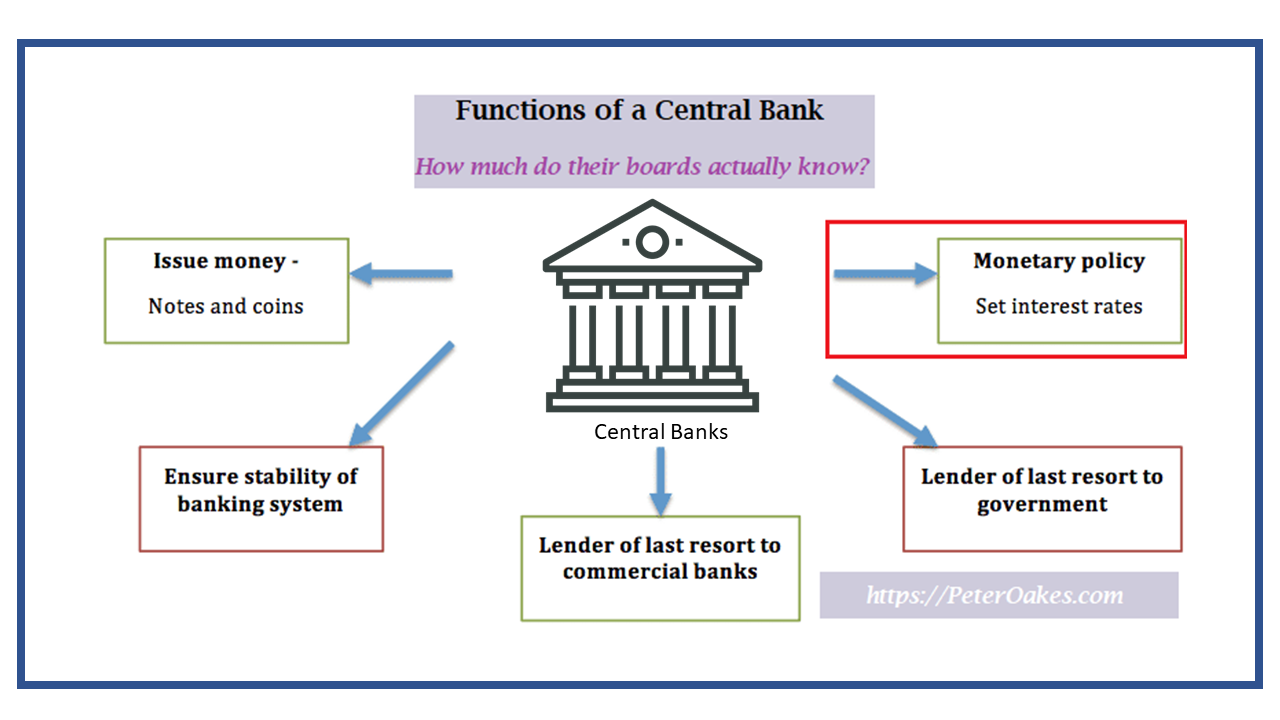

"Decision makers seem hostile to a consideration of evidence or research". This post relates to the Reserve Bank of Australia board, which has been lashed by a former researcher for failing to understand monetary policy in an email made public. Many of the points raised could be levied at other central banks too. As central banks continue to claim immunity from scrutiny under a misguided cloak of a widely misunderstood principle of 'central bank independence', which applies to some but not each and every aspect of a central bank's remit, we should expect to see more criticism of them particularly:

On the 2nd last point, it is welcome reading that in the case of the Australian central bank the damning email was released by the bank following a freedom of information request. This is not something one could expect from many European central banks. The email also criticised the central bank for:

Here's a link to the Australia article on Reserve Bank Here's the link to Stefan Gerlach's (former Central Bank of Ireland deputy governor) post on his 'lonesome battle against the incantations' Both are worth a read. And when you do, think about any relevance to your central bank and although there is always two sides to every story, in the absence of comment by the Australian central bank, the reports of Dr Peter Tulip's comments make for compelling reading and thinking. This article is reference in my post on Linkedin.

Back to Blog

Access White Paper Here

In the not too distant past, senior management within financial institutions may have regarded failure to comply with anti-money laundering (AML) requirements as low impact. The 2007/8 financial crisis as well as subsequent scandals in financial services have shown the error of this approach. When it comes to AML, the current COVID-19 crisis may pose an evolving and unpredictable threat. To avoid a repetition of the previous mistakes, financial institutions must now put into practice lessons learned from the past; the most urgent one in my book, is that institutions should be adopting a culture of compliance with a ‘live and breathe’ approach to regulatory requirements. In a recent article in the Economist, Jürgen Stock, secretary-general of Interpol, was quoted as saying that COVID-19 may create the ideal conditions for the spread of serious, organised crime. Moreover, Mr. Stock believes that the immanent global economic depression will offer these criminals a chance to extend their reach deep into the legitimate economy. As COVID-19 motivates criminals to evolve their operations, those responsible for stanching the flow of ill-gotten gains into the legitimate economy must stay one step ahead; and this includes financial institutions with their AML obligations. I recently published a white paper on the lessons to be learned from the last financial crisis. For those interested in how a culture of compliance can address complex misconduct relating to AML, this paper is well worth a read. Through reviewing a number of high-profile case studies, I come to the conclusion that at the heart of many AML failures is an institutional culture that treats AML training and procedures as merely means to meet regulatory requirements. The case studies show that these banks failed to ‘live and breathe’ regulatory requirements and that the institutional culture prioritised compliance as merely a tick the box exercise, thereby failing to communicate to employees the priority of compliance and the flexibility of decision making and behaviour that may be necessary to fulfil their AML requirements. Culture is a complex issue. For those interested in how RegTech can enable an examination of institutional culture, through diagnostic tools, the white paper is a must read. In the paper, I explore how The Mizen Group, a RegTech firm based in New York, has developed a suite of tools to help boards and their compliance officers assess the extent to which their institution demonstrates the characteristics of an organisation with a strong compliance culture. The financial crime threats posed by COVID-19 mean that now is the time to commit to a culture of compliance from the ground up. Launderers and criminals are capitalising on the chaos created in the wake of the pandemic and are seeking ways to out-manoeuvre the financial institutions who are generally playing catchup. In response, board of directors and executive management need to be proactive and flexible in their thinking and develop a ‘live and breathe compliance’ mentality. This will only occur in a healthy compliance culture, wherein employees are empowered to internalise the importance of complying for the right reasons. The first step towards the goal of a healthy compliance culture might be employing tools like Mizen’s innovative culture diagnostics to assess their institutions’ cultural strengths and weaknesses. Feel free to contact the RegTech experts at The Mizen Group for further information. Access White Paper Here This blog also appears at https://complireg.com/blogs--insights.html

Back to Blog

CompliReg, supporters of the Fintech Ireland Map, has written a short blog on the announcement (10th August 2020) that the Irish Government Cabinet has approved the publication of new draft rules which, if passed by both houses of Ireland's parliament, will strengthen existing Irish money laundering and terrorist financing laws to bring Ireland further into compliance with the 5th AML/CTF Directive.

Readers may recall that in July 2020, together with Romania, Ireland was fined €2 million for its delay in implementing the necessary legal changes to give effect to the 5th AML/CTF Directive. The blog is particularly relevant for regulated #Fintech firms, such as payment services and emoney firms, and the soon to be captured cryptoasset / cryptocurrency / cryptoexchange / cryptowallet providers operating from Ireland. More here - https://complireg.com/blogs--insights/new-irish-anti-money-laundering-rules-approved-by-government

Back to Blog

Ireland did not give Apple illegal State Aid. Wins round two in its fight with European Commission15/7/2020 Europe’s second-highest court rules today Ireland (through its tax authorities) did not give Apple illegal state aid. This overturns a European Commission decision 4 years’ ago that the iPhone maker owed the Irish taxman €13.1 billion in back taxes. Below is a text version of the PDF press release. General Court of the European Union PRESS RELEASE No 90/20 Luxembourg, 15 July 2020"General Court of the European Union Q PRESS RELEASE No 90/20 Luxembourg, 15 July 2020 Judgment in Cases T-778/16. Ireland v Commission, and T-892/16, Apple Sales International and Apple Operations Europe v Commission The General Court of the European Union annuls the decision taken by the Commission regarding the Irish tax rulings in favour of Apple The General Court annuls the contested decision because the Commission did not succeed in showing to the requisite legal standard that there was an advantage for the purposes of Article 107(1) TFEU[1] In 2016 the Commission adopted a decision[2] concerning two tax rulings issued by the Irish tax authorities (Irish Revenue) on 29 January 1991 and 23 May 2007 in favour of Apple Sales international (ASI) and Apple Operations Europe (AOE), which were companies incorporated in Ireland but not tax resident in Ireland. The contested tax rulings endorsed the methods used by ASI and ACE to determine their chargeable profits in Ireland, relating to the trading activity of their respective Irish branches. The 1991 tax ruling remained in force until 2007, when it was replaced by the 2007 tax ruling. The 2007 tax ruling then remained in force until Apple‘s new business structure was implemented in Ireland in 2014. By its decision, the Commission considered that the tax rulings in question constituted State aid unlawfully put into effect by Ireland. The aid was declared incompatible with the internal market. The Commission demanded the recovery of the aid in question. According to the Commission’s calculations, Ireland had granted Apple 13 billion euro in unlawful tax advantages.[3] Ireland (Case T-778116) and ASI and AOE (Case T-892/16) claimed that the General Court should annul the Commission's decision. By today‘s judgment, the General Court annuls the contested decision because the Commission did not succeed in showing to the requisite legal standard that there was an advantage for the purposes of Article 107(1) TFEU. According to the General Court, the Commission was wrong to declare that ASI and AOE had been granted a selective economic advantage and. by extension, State aid. The General Court endorses the Commission's assessments relating to normal taxation under the Irish tax law applicable in the present instance, in particular having regard to the tools developed within the OECD. such as the arm’s length principle. in order to check whether the level of chargeable profits endorsed by the Irish tax authorities corresponds to that which would have been obtained under market conditions. However. the General Court considers that the Commission incorrectly concluded, in its primary line of reasoning. that the lrish tax authorities had granted ASI and AOE an advantage as a result of not having allocated the Apple Group intellectual property licences held by ASI and ACE. and. consequently, all of ASI and AOE's trading income, obtained from the Apple Group's sales outside North and South America, to their Irish branches. According to the General Court, the Commission should have shown that that income represented the value of the activities actually carried out by the Irish branches themselves, in view of. inter alia. the activities and functions actually performed by the Irish branches of ASI and AOE, on the one hand, and the strategic decisions taken and implemented outside of those branches. on the other. In addition, the General Court considers that the Commission did not succeed in demonstrating, in its subsidiary line of reasoning, methodological errors in the contested tax rulings which would have led to a reduction in ASI and AOE's chargeable profits in Ireland. Although the General Court regrets the incomplete and occasionally inconsistent nature of the contested tax rulings, the defects identified by the Commission are not, in themselves, sufficient to prove the existence of an advantage for the purposes of Article 107(1) TFEU. Furthermore. the General Court considers that the Commission did not prove, in its alternative line of reasoning. that the contested tax rulings were the result of discretion exercised by the Irish tax authorities and that, accordingly, ASI and ACE had been granted a selective advantage. NOTE: An appeal, limited to points of law only, may be brought before the Court of Justice against the decision of the General Court within two months and ten days of notification of the decision. NOTE: An action for annulment seeks the annulment of acts of the Institutions of the European Union that are contrary to EU law The Member States the European Institutions and individuals may under certain conditions. bring an action for annulment before the Court of Justice or the General Court If the action Is well founded the act is annulled. The Institution concerned must fill any legal vacuum created by the annulment Unofficial document for media use, not binding on the General Court. The full text of judgement is published on the CURIA website on the day of delivery. [1] Article 107(1) TFEU ‘Save as otherwise provided In the Treaties any aid granted by a Member State or through State resources in any form whatsoever which distorts or threatens to distort competition by favouring certain undertakings or the production of certain goods shall, In so far as It affects trade between Member States. be incompatible with the Internal market [2] Commission Decision (EU) 2017/1283 01 30 August 2016 on State and SA 38673 (2014/0) (ex 2014/NN) (ex 2014/CP) Implemented by Ireland to Apple (notified under document C(2017) 5605) [3] Commission press release of 30 August 2016 State and Ireland gave illegal tax benefits to Apple worth up to 13 billion euro.

|

© Peter Oakes (all rights reserved)

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.